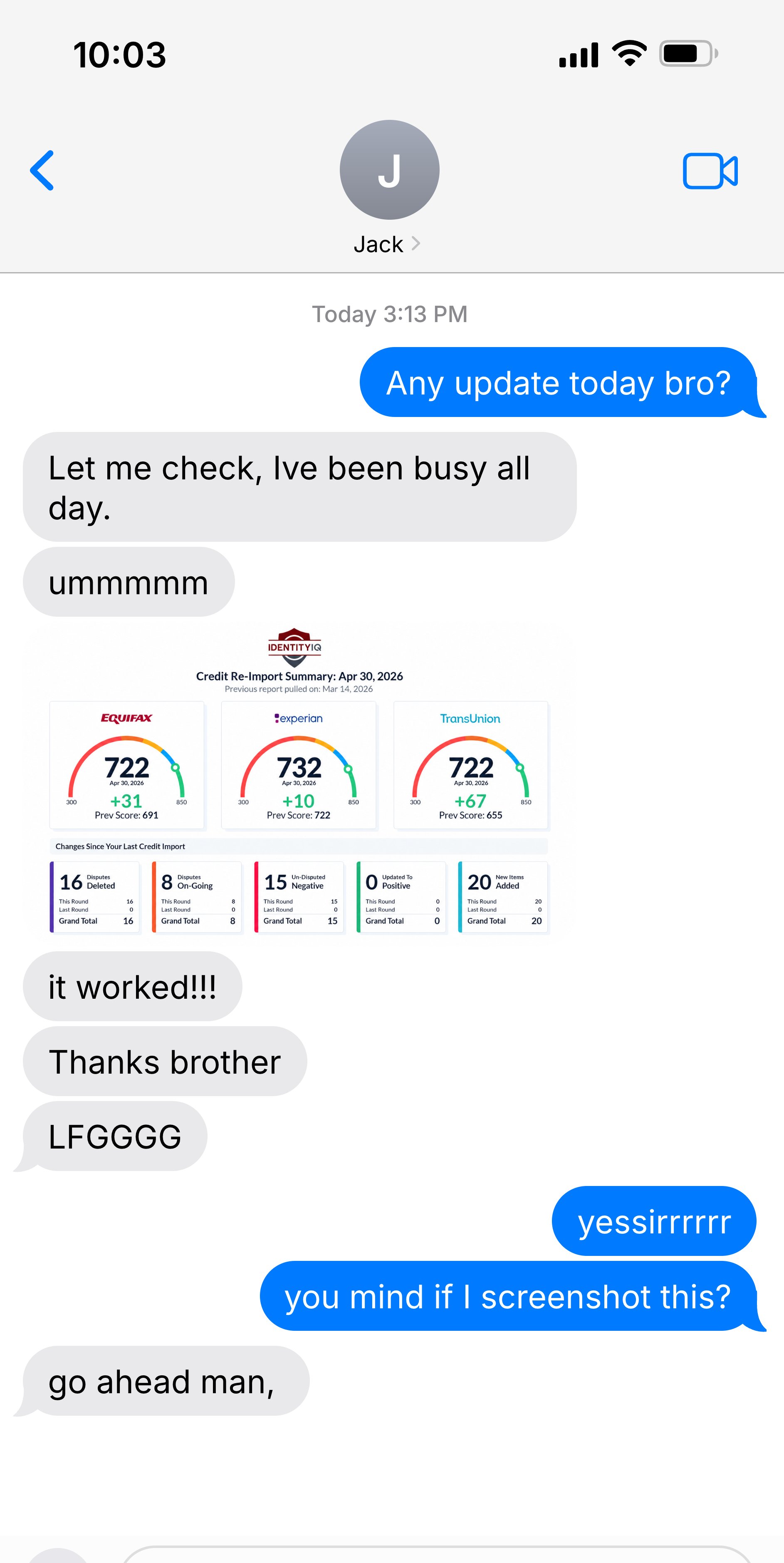

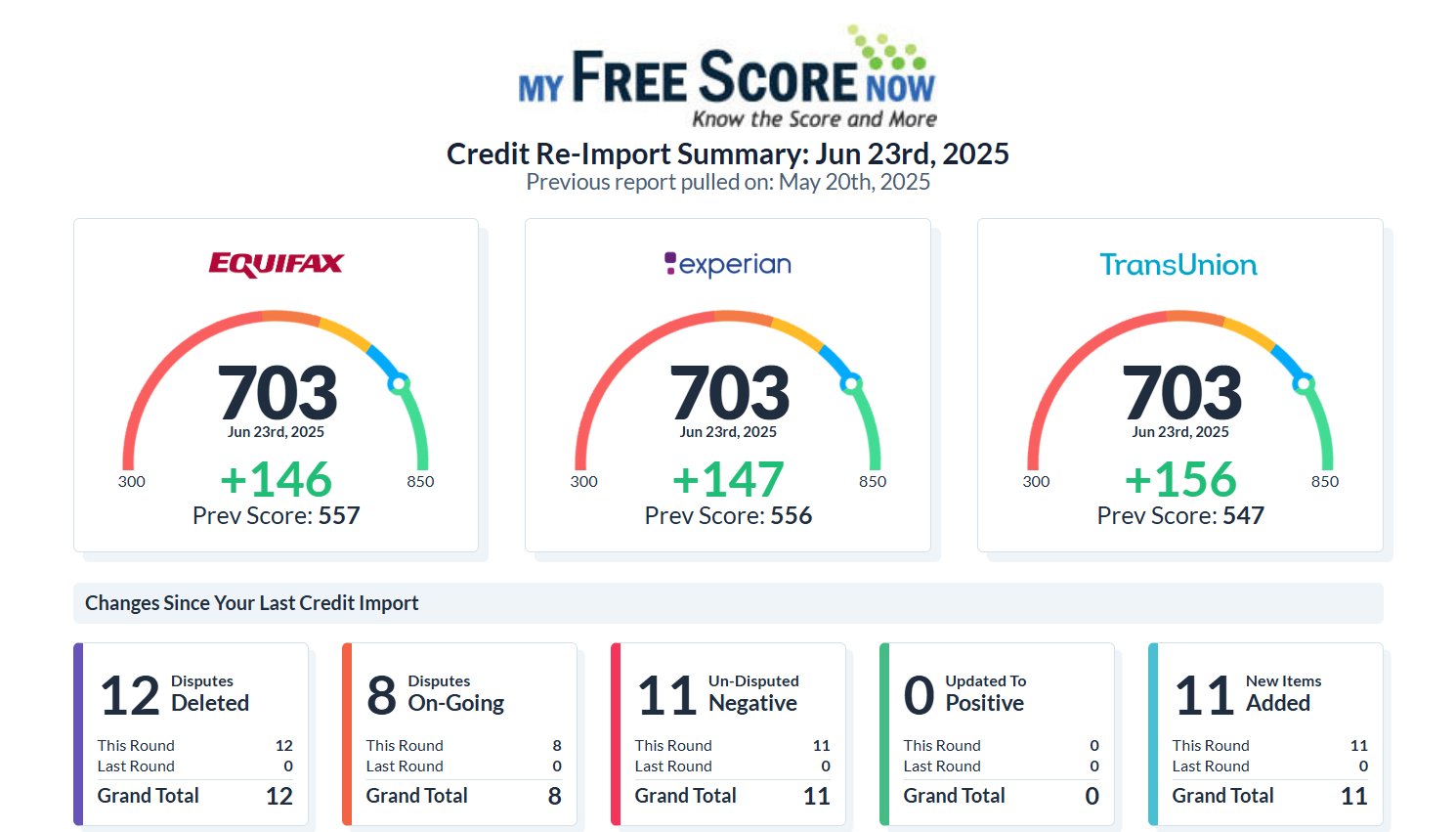

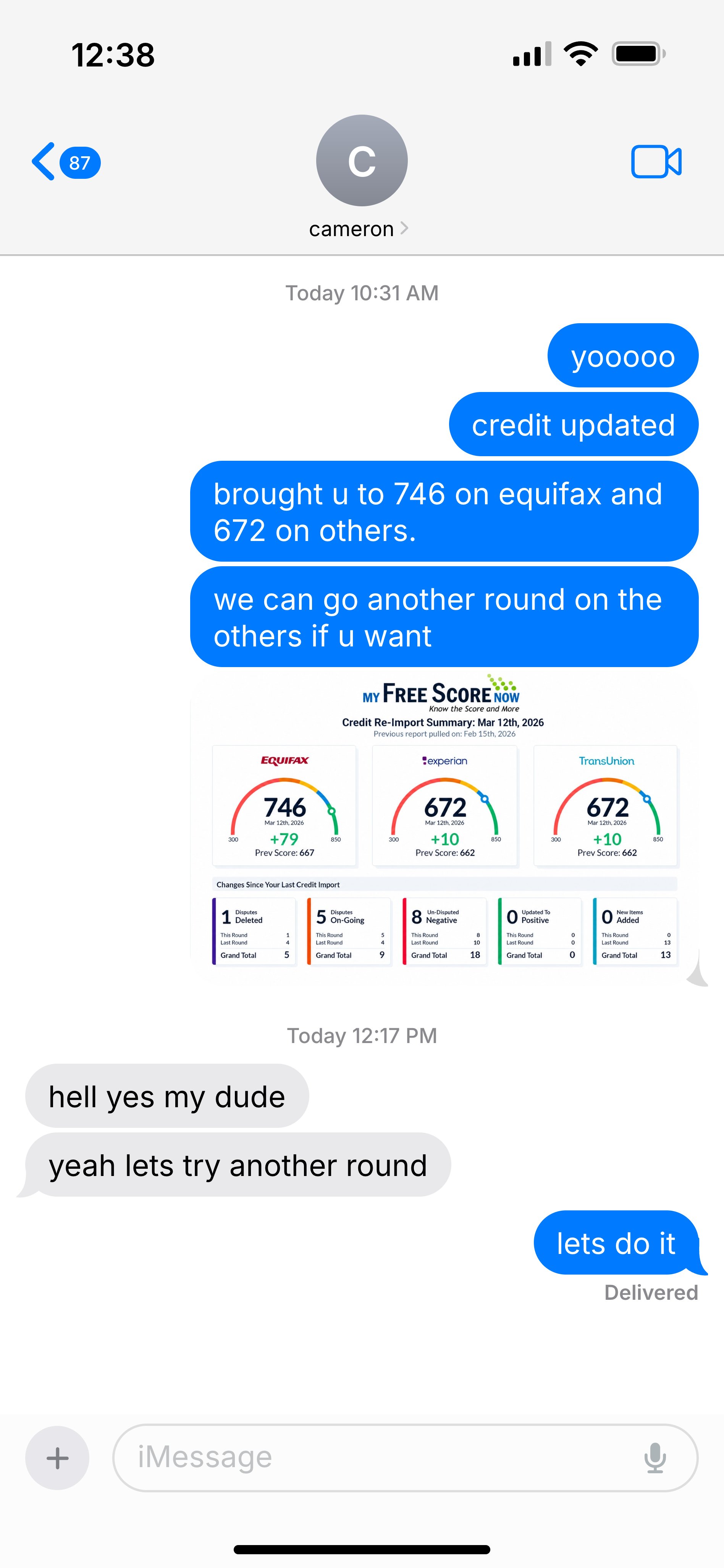

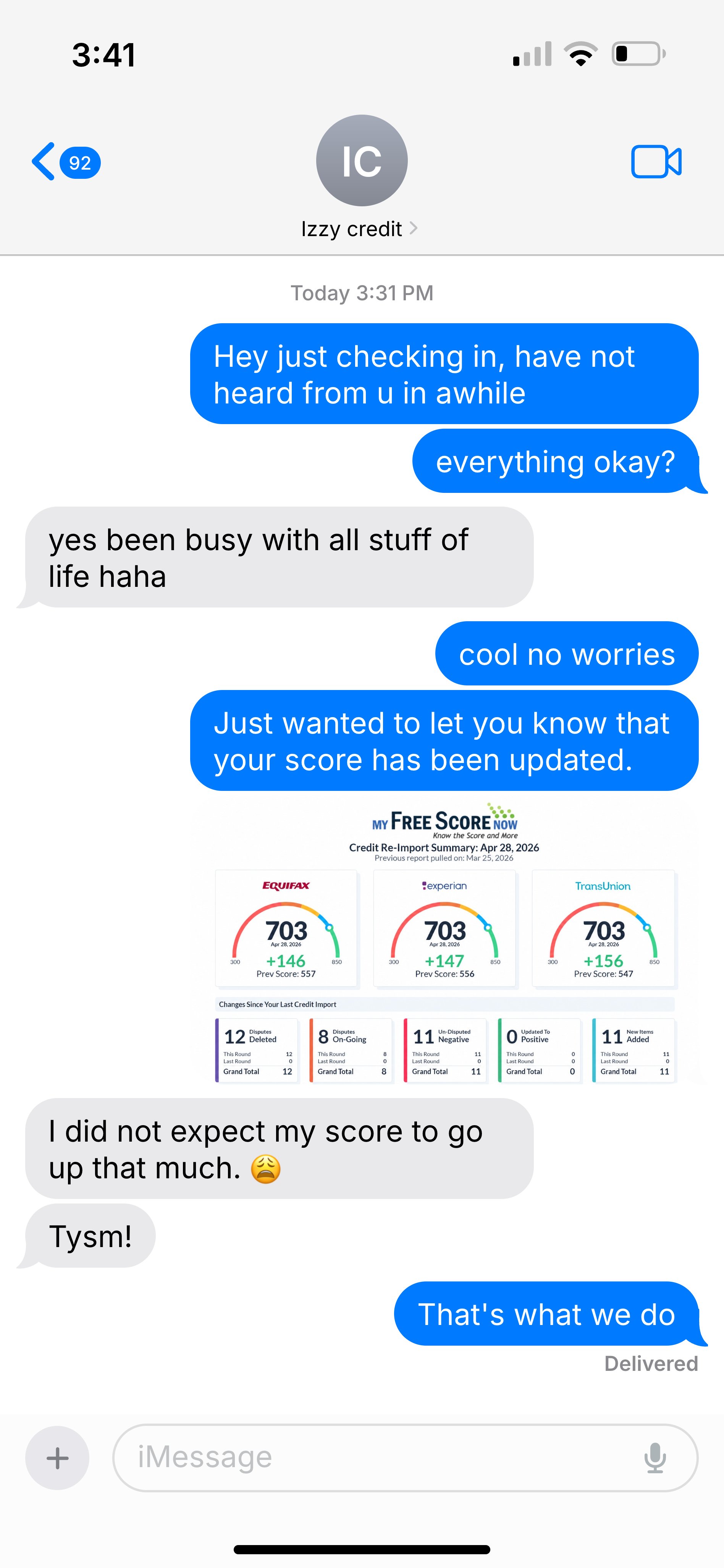

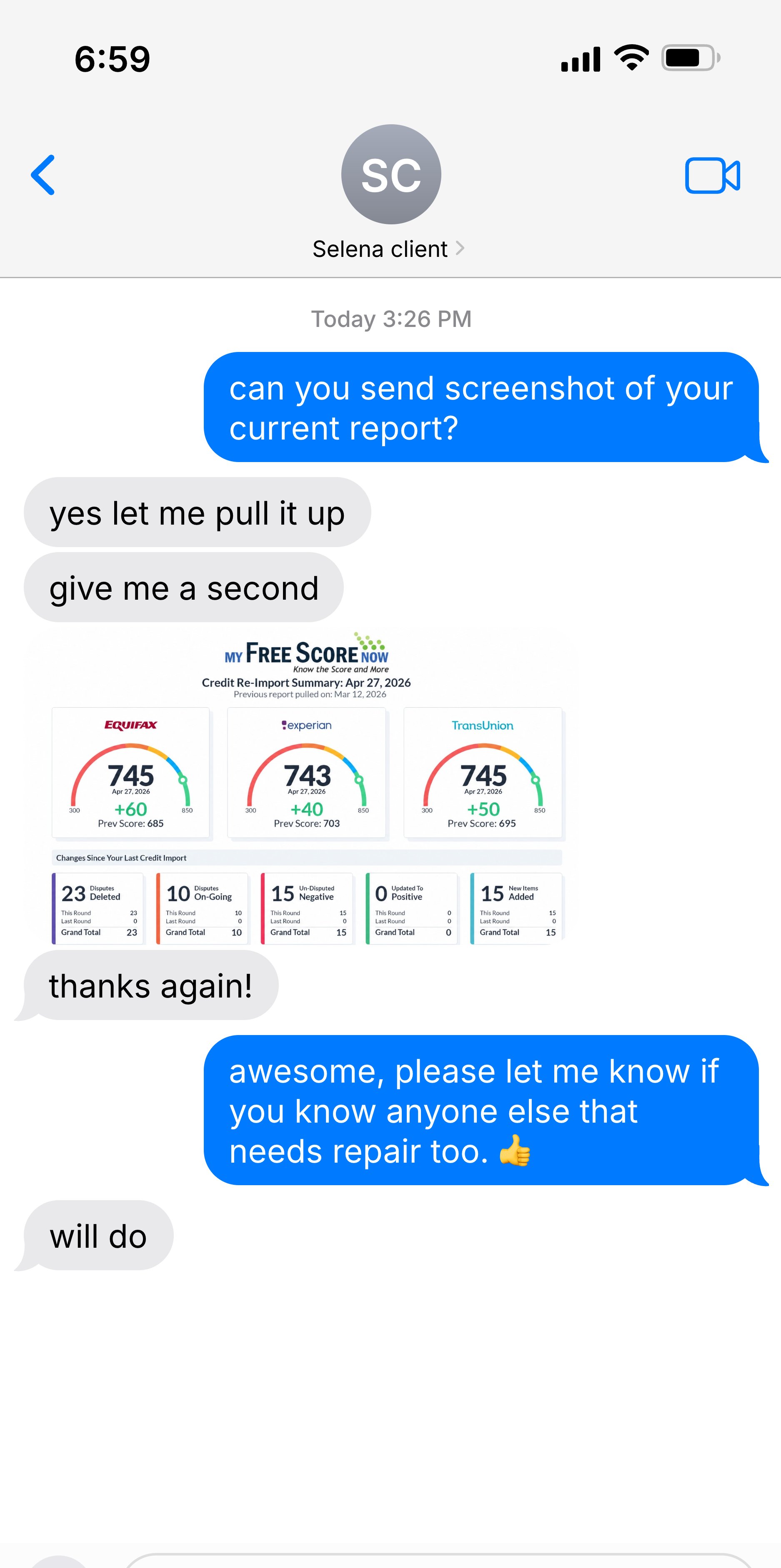

Real Wins. Real Results.

Individual results vary. Past results do not guarantee future outcomes. Screenshots used with explicit client consent.